Y1 21) What is Allocative Efficiency?

EconplusDal・11 minutes read

In a free market equilibrium, efficient resource allocation happens at the intersection of supply and demand, maximizing societal surplus when marginal private costs equal marginal private benefits. This efficiency is contingent upon several assumptions, and deviations from these lead to market failures, resulting in inefficient resource distribution.

Insights

- In a free market, efficient resource allocation happens at the point where supply meets demand, known as equilibrium, which maximizes societal benefits by ensuring that the cost of producing goods matches the benefits consumers receive. This balance is crucial because any shift away from this point leads to a loss in overall welfare, highlighting the importance of maintaining market conditions that support this equilibrium.

- Achieving allocative efficiency relies on several key conditions, including the presence of many buyers and sellers, perfect information, and the absence of barriers to market entry or exit. If these conditions are not met, market failures can arise, causing a gap between what is privately optimal for producers and consumers and what is socially optimal, ultimately resulting in ineffective use of resources.

Get key ideas from YouTube videos. It’s free

Recent questions

What is allocative efficiency?

Allocative efficiency refers to a state in a market where resources are distributed in such a way that maximizes the total benefit received by all participants in the economy. This occurs at the equilibrium point where the quantity of goods supplied equals the quantity demanded, ensuring that the price reflects both the marginal cost of production and the marginal benefit to consumers. At this point, the sum of consumer and producer surplus is maximized, meaning that no additional gains can be made without making someone worse off. In essence, allocative efficiency ensures that resources are used where they are most valued, leading to optimal production and consumption levels.

How do supply and demand curves work?

Supply and demand curves are fundamental concepts in economics that illustrate how the quantity of goods supplied and demanded varies with price. The supply curve typically slopes upward, indicating that as prices increase, producers are willing to supply more of a good to cover higher marginal costs associated with production. Conversely, the demand curve slopes downward, reflecting that as prices decrease, consumers are willing to purchase more of a good due to the increasing marginal utility they derive from each additional unit consumed. The interaction of these curves determines the market equilibrium price and quantity, where the amount supplied equals the amount demanded, facilitating efficient resource allocation.

What causes market failures?

Market failures occur when the assumptions necessary for a free market to function efficiently are violated, leading to inefficient resource allocation. Key factors that can cause market failures include the presence of monopolies or oligopolies, which limit competition; information asymmetries, where one party has more or better information than the other; externalities, which are costs or benefits incurred by third parties not involved in a transaction; and public goods, which are non-excludable and non-rivalrous, leading to underproduction. When these conditions exist, the market may not reach an equilibrium where marginal social costs equal marginal social benefits, resulting in a loss of welfare and suboptimal outcomes for society.

What are marginal private costs?

Marginal private costs refer to the additional costs incurred by producers when they produce one more unit of a good or service. These costs include direct expenses such as wages, materials, utilities, and rent, and they typically increase with each additional unit produced due to the law of diminishing marginal returns. As production expands, the cost of inputs may rise, leading suppliers to require higher prices to cover these increased costs. Understanding marginal private costs is crucial for firms as they make production decisions, as it directly influences their pricing strategies and overall profitability in a competitive market.

What is the significance of equilibrium in economics?

Equilibrium in economics is a critical concept that represents a state where supply equals demand, resulting in a stable market condition. At this point, the price of goods reflects the true cost of production and the value consumers place on them, leading to an efficient allocation of resources. The significance of equilibrium lies in its ability to maximize total welfare, as it ensures that the sum of consumer and producer surplus is at its highest. Deviations from this equilibrium can lead to market inefficiencies, such as surpluses or shortages, which can disrupt the balance and result in welfare losses. Thus, understanding equilibrium is essential for analyzing market dynamics and the overall health of an economy.

Related videos

Marginal Revolution University

The Equilibrium Price and Quantity

Srijan India One

Microeconomics | Chapter 5| Class 12 | Srijan India

Rajat Arora

Day 8 | Micro economics | Consumer's Equilibrium | Chapter 2 | One Shot

EconClips

💱 Price System | Free Market vs. Government Intervention

DrAzevedoEcon

Chapter 1: Ten Principles of Economics

Summary

00:00

Understanding Free Market Equilibrium Dynamics

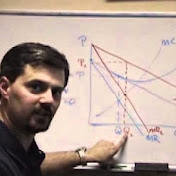

- In a free market equilibrium, efficient allocation of scarce resources occurs at the intersection of supply and demand, represented by P star (price) and Q star (quantity), where marginal private costs equal marginal private benefits, ensuring maximum societal surplus.

- The supply curve reflects the marginal private costs of production, which include expenses such as gas, electricity, wages, and rent. These costs increase with each additional unit produced due to the law of diminishing marginal returns, leading suppliers to require higher prices to cover these costs.

- The demand curve represents the marginal private benefits to consumers, which decrease with each additional unit consumed due to the law of diminishing marginal utility, resulting in a downward-sloping demand curve.

- Allocative efficiency is achieved when the sum of consumer and producer surplus is maximized, occurring at equilibrium where demand equals supply (P star and Q star). Any deviation from this equilibrium results in a loss of welfare.

- The maximization of net social benefit occurs at equilibrium when marginal social costs equal marginal social benefits, ensuring that the production of goods continues until the cost of producing an additional unit equals the benefit derived from it.

- For a free market to achieve allocative efficiency, key assumptions must hold: there must be many buyers and sellers, perfect information for all parties, no barriers to entry or exit for firms, and both firms and consumers must act as profit and utility maximizers, respectively.

- If any of these assumptions are violated, market failures can occur, leading to discrepancies between private optimum (where supply equals demand) and social optimum (where marginal social costs equal marginal social benefits), resulting in inefficient resource allocation.