Microeconomics | Chapter 5| Class 12 | Srijan India

Srijan India One・78 minutes read

Market equilibrium is the balance of demand and supply, with price ceilings and floors set by the government to control prices. The equilibrium price and quantity are determined by aligning consumer and firm plans in the market.

Insights

- Market equilibrium is the point where demand and supply are balanced, ensuring that consumers are willing to purchase a specific quantity at various prices, and firms are willing to supply that quantity. Equilibrium price and quantity are crucial for a balanced market, determined by the intersection of demand and supply curves.

- Price ceilings and floors, established by the government, impact market equilibrium by controlling prices. Price ceiling sets a maximum price to keep goods affordable, while price floor establishes a minimum price to maintain market stability. These interventions can lead to shortages or surpluses, affecting consumer satisfaction and market dynamics.

Get key ideas from YouTube videos. It’s free

Recent questions

What is market equilibrium?

Market equilibrium is the point where demand and supply are balanced, ensuring optimal levels for both.

How do price ceilings impact markets?

Price ceilings set by the government control prices to keep them below market rates, aiming to make goods affordable.

What is the invisible hand concept?

The invisible hand concept, introduced by Adam Smith, plays a crucial role in restoring market equilibrium by guiding self-interested individuals towards the common good.

How does an increase in consumer income affect market equilibrium?

An increase in consumer income leads to higher demand for goods, shifting the equilibrium point and impacting prices and quantities.

Why is equilibrium price equal to minimum average cost?

Equilibrium price equals minimum average cost due to free entry and exit of firms, ensuring that firms earn normal profits in the long run.

Related videos

Marginal Revolution University

The Equilibrium Price and Quantity

Rajat Arora

Consumer's Equilibrium | Chapter 2 | Microeconomics | Part 3

EconplusDal

Y1 21) What is Allocative Efficiency?

EconClips

💱 Price System | Free Market vs. Government Intervention

Think Econ

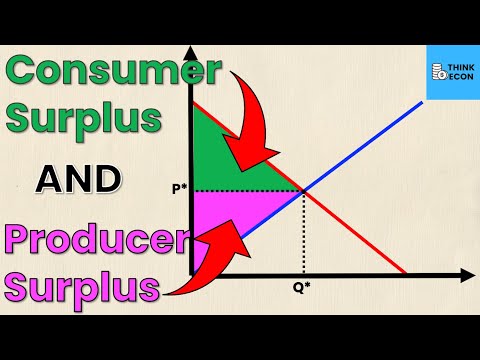

How to Calculate Producer Surplus and Consumer Surplus from Supply and Demand Equations | Think Econ

Summary

00:00

Achieving Market Equilibrium: Balancing Supply and Demand

- Market equilibrium is the point where everything is at its optimum level, balancing demand and supply.

- Equilibrium of demand is when consumers collectively are willing to purchase a certain quantity at different prices.

- Market equilibrium of supply occurs when the fixed number of firms or free entry and exit conditions are met.

- Price ceilings and floors, set by the government, impact the market equilibrium by controlling prices.

- Equilibrium is reached when the plans of all consumers and firms in the market align, leading to a balanced market.

- Equilibrium price is the price at which demand equals supply, ensuring market clearing.

- Equilibrium quantity is the amount sold at the equilibrium price, reflecting the balance between supply and demand.

- The invisible hand concept, introduced by Adam Smith, plays a crucial role in restoring market equilibrium.

- Access supply and demand occur when there is an imbalance in the market, prompting price adjustments to reach equilibrium.

- Market equilibrium with a fixed number of firms is achieved when supply and demand curves intersect, indicating a balanced market.

17:07

Market Equilibrium: Balancing Demand and Supply

- Equilibrium is crucial for determining the market situation.

- Price and quantity are interdependent; if one changes, the other follows suit.

- High prices lead to reduced demand, prompting a price reduction.

- Lower prices attract more buyers, increasing demand.

- Equilibrium is achieved when market demand equals market supply.

- Equilibrium price and quantity are determined by balancing demand and supply.

- The equilibrium price can be calculated using specific equations.

- Access demand and supply are essential to understand market dynamics.

- Wage determination in the labor market involves balancing demand and supply of labor.

- The downward-sloping demand curve in the labor market is influenced by wage rates.

31:59

"Wage Rates Impact Labor Demand and Equilibrium"

- Labor demand curve is derived based on wage rates and individual units supplied.

- Increase in wage rate leads to higher opportunity cost of laser activity.

- Higher wages result in individuals preferring to work more and enjoy less leisure activities.

- Increase in wage rate leads to higher purchasing power and increased spending on leisure activities.

- Impact of wage rate increase depends on the balance between opportunity cost and purchasing power effects.

- Shifts in demand and supply curves impact equilibrium prices and quantities.

- Increase in consumer income leads to higher demand for goods and shift in equilibrium.

- Normal goods see increased demand with higher consumer income, while inferior goods see reduced demand.

- Supply curve remains unchanged unless affected by factors like technology or production costs.

- Increase in number of consumers leads to higher demand for goods, affecting equilibrium prices and quantities.

47:25

Consumer and Firm Impact on Demand and Supply

- An increase in the number of consumers leads to a shift in the demand curve to the right.

- The equilibrium point also shifts upwards due to the increase in consumer numbers.

- The increase in the number of consumers does not affect the supply curve, only the demand curve.

- An increase in the number of firms leads to a shift in the supply curve, while the demand curve remains constant.

- The demand curve shifts downwards when the supply remains the same.

- The new equilibrium point changes due to the shift in the demand and supply curves.

- An increase in input prices results in a leftward shift in the supply curve.

- The increase in input prices does not impact consumer demand directly.

- The increase in input prices leads to a rise in market prices and a decrease in quantity produced.

- The entry of more firms leads to a rightward shift in the supply curve, with no effect on the demand curve.

01:03:02

Equilibrium Price and Quantity Dynamics in Markets

- Curve shift to the right results in increased quantity and price decrease

- Equilibrium quantity increases due to rightward shift in both demand and supply curves

- Price remains unchanged in equilibrium when quantity increases

- Price decreases due to leftward shift in demand

- Market equilibrium study focuses on fixed number of firms

- In equilibrium, no firm earns super normal profit or incurs loss

- Equilibrium price equals minimum average cost of the firm

- Free entry and exit lead to firms earning super normal profits initially

- With sufficient number of firms, profit levels out to normal profit

- Equilibrium price is always equal to minimum average cost due to free entry and exit of firms

01:18:48

Government Sets Price Limits to Regulate Markets

- Price ceiling and floor prices are set by the government to regulate the prices of goods and services.

- Price ceiling is an upper limit imposed by the government on certain goods like wheat, rice, kerosene, and sugar.

- Price ceiling aims to keep prices below the market determined price to make goods affordable, like in ration shops.

- The government imposes price ceiling to prevent prices from rising excessively, leading to increased demand and shortages.

- Price ceiling can result in shortages and dissatisfaction among consumers due to limited availability of goods.

- Price floor, on the other hand, is a minimum price set by the government for goods and services, like in agricultural price support programs.

- Price floor prevents prices from falling below a certain level, ensuring stability in the market.

- Equilibrium in a competitive market is achieved when market demand equals market supply, determining the price and quantity of goods.