The Retirement Gamble (full documentary) | FRONTLINE

FRONTLINE PBS | Official・2 minutes read

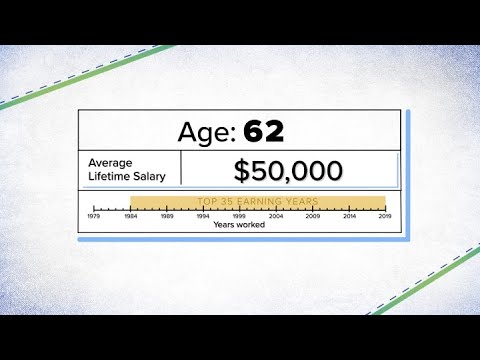

To retire comfortably, earning $100,000 annually requires $1.5 million, with many 401k programs failing participants and Americans borrowing from their retirement accounts due to financial difficulties. Social Security may not be enough for retirement, leading to longer working years and increased savings, as the burden shifts to individuals with transparency lacking in the 401k system.

Insights

- The shift from traditional pensions to 401k plans places the retirement burden on individuals, with many programs being deemed inadequate, leading to participants bearing risks and receiving only a fraction of returns.

- High fees and lack of transparency in retirement accounts, as highlighted by individuals like Robert Hilton Smith and Crystal Mendes, significantly impact savings, with financial firms prioritizing profits over clients' interests, advocating for simpler, low-cost investment approaches like index funds.

Get key ideas from YouTube videos. It’s free

Recent questions

How much money do I need to retire comfortably?

To retire comfortably, if you earn $100,000 annually, you need $1.5 million.

Are 401k programs sufficient for retirement savings?

Many 401k programs are deemed inadequate, with participants bearing the risk and receiving only 30% of the returns.

How do high fees impact retirement savings?

High fees in retirement accounts significantly impact individuals' savings.

What is the role of Social Security in retirement planning?

Social Security may not suffice for retirement, leading many to work longer and save more.

How can individuals improve their retirement outcomes?

Individuals can improve their retirement outcomes by minimizing fees, investing in low-cost index funds, and prioritizing long-term financial goals.

Related videos

Summary

00:00

Retirement Savings Challenges and Strategies

- To retire comfortably, if you earn $100,000 annually, you need $1.5 million.

- Many 401k programs are deemed inadequate, with participants bearing the risk and receiving only 30% of the returns.

- Americans are increasingly borrowing from their retirement accounts due to financial struggles.

- Half of Americans cannot afford to save for retirement, with the average retirement fund losing $12,000.

- Social Security may not suffice for retirement, leading many to work longer and save more.

- The shift from traditional pensions to 401k plans places the retirement burden on individuals.

- The mutual fund industry capitalized on the 401k trend, making mutual funds a core component.

- The 401k system lacks transparency, with individuals often unaware of fees and risks.

- The dot-com era saw significant growth in the stock market, leading to inflated retirement savings.

- The market crash in 2000 resulted in substantial losses for many, with some losing a significant portion of their retirement savings.

17:03

401k Fees Impact Retirement Savings and Outcomes

- Debbie Skedzinski worked for Com Disco, a computer leasing company, and had close to half a million dollars in her 401k with company stock.

- Due to dot-com failures, Skedzinski lost her savings and job as the company filed for bankruptcy protection, leading to 200 job cuts.

- Concerns about shaky home mortgages triggered fears of a financial meltdown, impacting savers like Skedzinski.

- Skedzinski's house was worth less than her loan, leading her to dip into her 401k, like a quarter of Americans have done.

- Wall Street bonuses during the market crash raised outrage, with $18 billion in bonuses distributed.

- Robert Hilton Smith, an economics graduate, discovered high fees in his 401k, affecting his returns.

- Smith found various fees in his investment options, including asset management, trading, and administrative fees.

- Jack Bogle emphasized minimizing fees to improve retirement outcomes, highlighting the impact of compound costs.

- Crystal Mendes discovered high fees and surrender fees in her retirement account, prompting her to reconsider her investments.

- The industry's lack of transparency on fees and kickbacks to brokers adds layers of costs to retirement plans, impacting individuals' savings significantly.

33:34

"Index Funds: A Safer Investment Approach"

- Hilton Smith criticized financial firms for charging high fees with minimal returns, advocating for a simpler and safer investment approach.

- Jack Bogle has promoted long-term, low-cost investing through index funds, emphasizing owning American businesses with minimal trading and management fees.

- Index funds hold a diversified basket of stocks, matching market indexes like the S&P 500, with a cost of one percent annually.

- Actively managed mutual funds have consistently failed to outperform index funds over various time periods.

- Financial advisors often recommend actively managed funds despite evidence showing index funds perform better.

- The lack of clear standards on financial advice leads to confusion for consumers, with many advisors not acting as fiduciaries.

- Salespeople often prioritize their profits over clients' interests, selling products like annuities with hidden fees and lower returns.

- The Department of Labor proposed a fiduciary rule to prioritize clients' interests in retirement accounts, facing opposition from the financial services industry.

- Despite efforts to reform the industry, the retirement savings system remains complex and challenging for many Americans.

- Individuals have mixed feelings about their retirement prospects, with some confident in their investment strategies while others express worry and uncertainty about their financial future.

50:47

"America's Retirement Crisis: Funding Challenges and Calculators"

- Retirement planning is a challenge, with individuals like Hilton Smith researching America's retirement crisis while struggling to secure grant funding. Personal experiences with online retirement calculators vary from optimistic to discouraging, emphasizing the need to save more than expected for retirement.